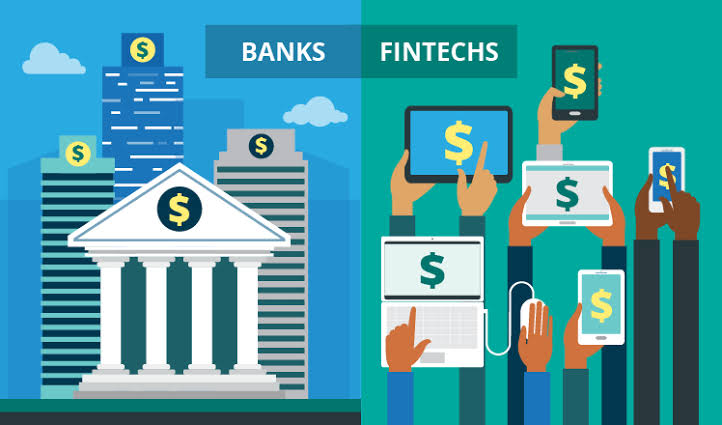

The emergence of fintech companies around the world has disrupted the traditional banking sector due to its rapid pace of digital acceleration.

However, for decades, banks have acted as reliable financial institutions for their customers and have made the best use of the benefits of their data by increasing their revenue and profits in the long run.

Nigeria is currently experiencing a shift in technological advancement. From the rise of startups to various fintech companies dominating the economic climate, it is rapidly heading into the mobile-only community where the internet has become an extension of a person like digital money, e-wallets and cashless transactions.

Innovators are thinking big and taking advantage of the country’s growing echosystem and its tech-savvy population.

Although traditional banks have been thriving for a long time, the strong relationships they have with their customers come with unnecessary additional costs. This increases the demand for individuals to easily access the services they need through easy-to-use digital methods.

Now, with fintech continuing to establish itself across the country, is there anything our traditional banks can do to keep up?

The competition between the traditional banking sector and fintech still thrives However, it is unlikely that fintech startups will completely replace our banks.

There is no doubt that due to the strong wave of digitization, banks are becoming more vulnerable. They are gradually losing market shares to technology companies that have already established themselves as players in financial services.

Fintech companies like PiggyVest, Interswitch, Flutter Wave, Kuda Bank, Paystack, and many others are innovating past traditional institutions by making digital financial services like lending, saving and investing easily available to people.

Since these disruptors can withstand the competition at lower costs to customers, banks are more likely to lose margins when their services become a commodity. If they want to survive, they must start acting and thinking like digital giants.

How Can Banks Rise to The Top?

In an article published by Forbes, a 2018 global banking study reveals that the most important way to acquire, engage and retain customers is to provide them with the technology-based tools they want.

In order for banks to remain competitive, they must become more innovative and embrace new technology again.

However, traditional banks still have a huge advantage for the in-house interface. Despite the fact that technology offers a lot, many individuals still prefer human interaction to help them in complex transactions.

Banks are still trusted by a large part of their customers, thanks to their reliable record of keeping personal data. This foundation of trust gives them an edge over technology platforms, which they can take advantage of to stay relevant.

For traditional banks to enhance their customer experience, they need to understand how fintech disruption is occurring in the industry. Fintech companies offer cheaper and faster products within a short period of time.

Banks that fail to adapt to today’s technology can be difficult to deal with, expensive to manage and inaccessible to consumers who demand digital solutions.

Digital transformation is a major cultural programme.

Banks need to prepare their designers, data scientists, developers, and infrastructure to support new design models and connected experiences for consumers and employees because technology evolves every day.

They can embrace multi-currency fintech processing, one-click borderless payments and an AI-based security system, all of which can instantly offer customers a more comprehensive level of service.

By partnering with technology companies, they can make further improvements to the back office. It is increasingly common for banks to use cloud services offered by major technology companies. Therefore, establishing these practices will provide banks with a way to simplify their existing complex IT systems and generate savings.

If the country’s traditional banks can adopt most of these innovative ideas, they can help drive economic development by boosting financial productivity, improving access to financial services, and reducing income inequality.

{kind=link}